Last year marked the 90th anniversary of the Social Security Act being signed into law by President Franklin D. Roosevelt. Since the first retired-worker benefit was mailed in January 1940, Social Security has been providing a financial foundation for aging workers who could no longer do so for themselves.

In May 2025, we also witnessed the average monthly retired-worker benefit surpass $2,000 for the first time.

But not all history is shaping up as positive for America’s foremost retirement program. The financial outlook for Social Security has been deteriorating for decades, leading some workers to believe it won’t be there when they retire. While there’s a silver lining on this front and Social Security’s longevity as a whole, the existing payout schedule, including annual cost-of-living adjustments (COLA), is far from sturdy — and actions taken by President Donald Trump in July 2025 appear to have made things worse.

The president’s “Big, Beautiful Bill” has created a big, unsightly problem for America’s foremost retirement program.

Last year marked the 90th anniversary of the Social Security Act being signed into law by President Franklin D. Roosevelt. Since the first retired-worker benefit was mailed in January 1940, Social Security has been providing a financial foundation for aging workers who could no longer do so for themselves.

In May 2025, we also witnessed the average monthly retired-worker benefit surpass $2,000 for the first time.

But not all history is shaping up as positive for America’s foremost retirement program. The financial outlook for Social Security has been deteriorating for decades, leading some workers to believe it won’t be there when they retire. While there’s a silver lining on this front and Social Security’s longevity as a whole, the existing payout schedule, including annual cost-of-living adjustments (COLA), is far from sturdy — and actions taken by President Donald Trump in July 2025 appear to have made things worse.

President Trump addressing Congress. Image source: Official White House Photo.

Is Social Security going to run out of money? No… but that’s only part of the story.

For the last 85 years, the Social Security Board of Trustees has released an annual report detailing how the program generates income and where those dollars end up. This lengthy report also relies on changes in fiscal and monetary policy, along with demographic shifts, to project the financial health of Social Security over the long term (75 years after the report’s publication).

For four decades, the Trustees Report has warned of a long-term unfunded obligation. In plain English, the estimated income collected 75 years following a report is projected to be insufficient to cover outlays (benefits plus the administrative expenses to run Social Security). This unfunded obligation has ballooned to $25.1 trillion as of 2025.

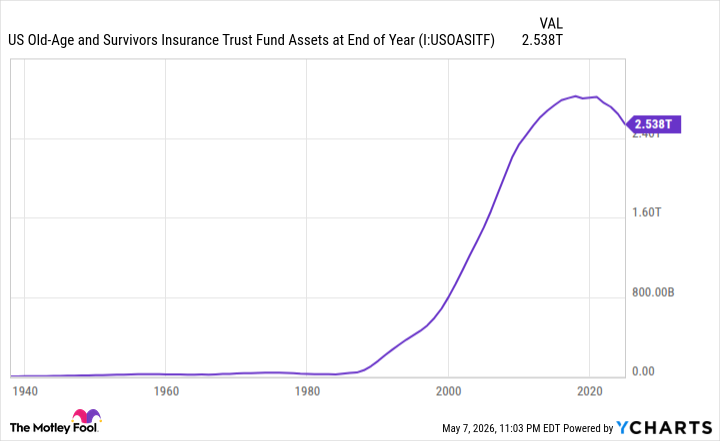

The bigger issue is the expected exhaustion of the Old-Age and Survivors Insurance trust fund’s (OASI) asset reserves by 2033. This is the fund responsible for paying monthly benefits to retired workers and the survivors of deceased workers.

The 2025 Trustees Report predicts that a depletion of the OASI’s asset reserves — the excess income collected since inception that’s invested in special-issue, interest-bearing government bonds, as required by law — will result in sweeping benefit cuts of up to 23% by 2033.

The OASI is projected to exhaust its asset reserves in the coming years. US Old-Age and Survivors Insurance Trust Fund Assets at End of Year data by YCharts.

If there’s a silver lining to this seemingly dire outlook, it’s that Social Security is no danger of becoming insolvent, going bankrupt, or halting benefits. Even without a penny in its asset reserves, the OASI can still pay benefits to eligible recipients, albeit at the aforementioned reduced rate.

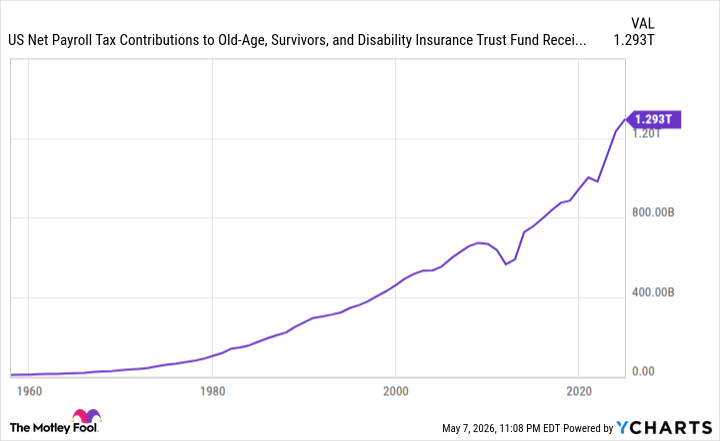

The way Social Security is funded ensures that it can’t go bankrupt or disappear. Its primary funding source, the 12.4% payroll tax on earned income (wages and salaries, but not investment income), generated over 91% of the $1.42 trillion collected in 2024. As long as workers continue to pay their taxes, the OASI will always have income to dole out to eligible beneficiaries.

Unless Congress amends the Social Security Act’s funding provisions, the program cannot go bankrupt. That’s the good news, but it doesn’t tell the full story of what’s (likely) to come.

Image source: Getty Images.

President Trump’s “Big, Beautiful Bill” has created a big, unsightly deficit for Social Security

For some taxpayers, President Trump’s “Big, Beautiful Bill,” signed into law in July 2025, has helped pad their pocketbooks. In addition to personal income tax bracket changes, the BBB, as Trump’s flagship tax and spending law is better known, instituted several temporary tax cuts from 2025 through 2028:

- The “senior deduction” allows eligible seniors aged 65 and above to take an additional $6,000 off of their taxable income ($12,000 for married couples filing jointly).

- The “no tax on overtime” provision enables workers to claim dollar-for-dollar deductions on overtime pay of up to $12,500 ($25,000 for jointly filing couples).

- The “no tax on tips” provision allows workers a dollar-for-dollar deduction of up to $25,000 in tips.

But Trump’s championed tax law isn’t having the same effect for America’s foremost retirement program.

As noted, the payroll tax is the primary funding vehicle for Social Security, with the federal taxation of benefits and the interest earned on asset reserves combining for less than 9% of income collected in 2024. Trump’s BBB is reducing the amount of earned income subject to the payroll tax from 2025 through 2028. Less payroll tax income means an even steeper funding deficit for Social Security.

The payroll tax accounts for the lion’s share of Social Security’s collected income. US Net Payroll Tax Contributions to Old-Age, Survivors, and Disability Insurance Trust Fund Receipts data by YCharts.

In late July 2025, the ranking member of the Senate Banking Committee, Ron Wyden (D-OR), requested that the Social Security Administration (SSA) analyze the projected 10-year impact of the BBB on the program. In early August, Wyden received a response from the SSA’s Office of the Actuary (OACT).

The OACT highlighted income shortfalls for the program from 2025 to 2034 that are expected to increase costs (i.e., widen the funding obligation shortfall) by $168.6 billion. Yes, this is a relatively small figure next to the Trustees’ forecasted long-term shortfall of $25.1 trillion, but it’s not a drop in the bucket, either.

According to the OACT, the BBB is projected to shift the OASI’s asset reserve depletion date forward by one quarter, to the fourth quarter of 2032 from the first quarter of 2033. In other words, the timeline to sweeping benefit cuts has been accelerated by President Trump.

Social Security’s money isn’t going to run out, but things could definitely get dicey for beneficiaries six years from now.