Lucid (NASDAQ:LCID) primarily designs, engineers, and builds electric vehicles, powertrains, and battery systems for consumers.

It entered a new leadership phase and expanded a commercial agreement, while recording approximately -364% net income margin for the quarter ended March 31, 2026.

Recent results reveal a stark contrast in revenue stability and margins between these two EV companies. See how their financial trajectories diverge.

Lucid: High Volatility in Recent Revenue Trends

Lucid (LCID 4.89%) primarily designs, engineers, and builds electric vehicles, powertrains, and battery systems for consumers.

It entered a new leadership phase and expanded a commercial agreement, while recording approximately -364% net income margin for the quarter ended March 31, 2026.

Tesla: Maintaining Massive Revenue Volume and Scale

Tesla (TSLA +3.87%) primarily designs, manufactures, and sells electric vehicles, alongside energy generation and storage systems.

It shifted its autonomous software to a monthly subscription format and launched a commercial trucking pilot, while generating approximately 2% net income margin for the quarter ended March 31, 2026.

Why Revenue Matters for Retail Investors

Revenue refers to the standardized income-statement revenue line item from company filings, and it shows investors the total amount of money the business brings in before expenses are deducted.

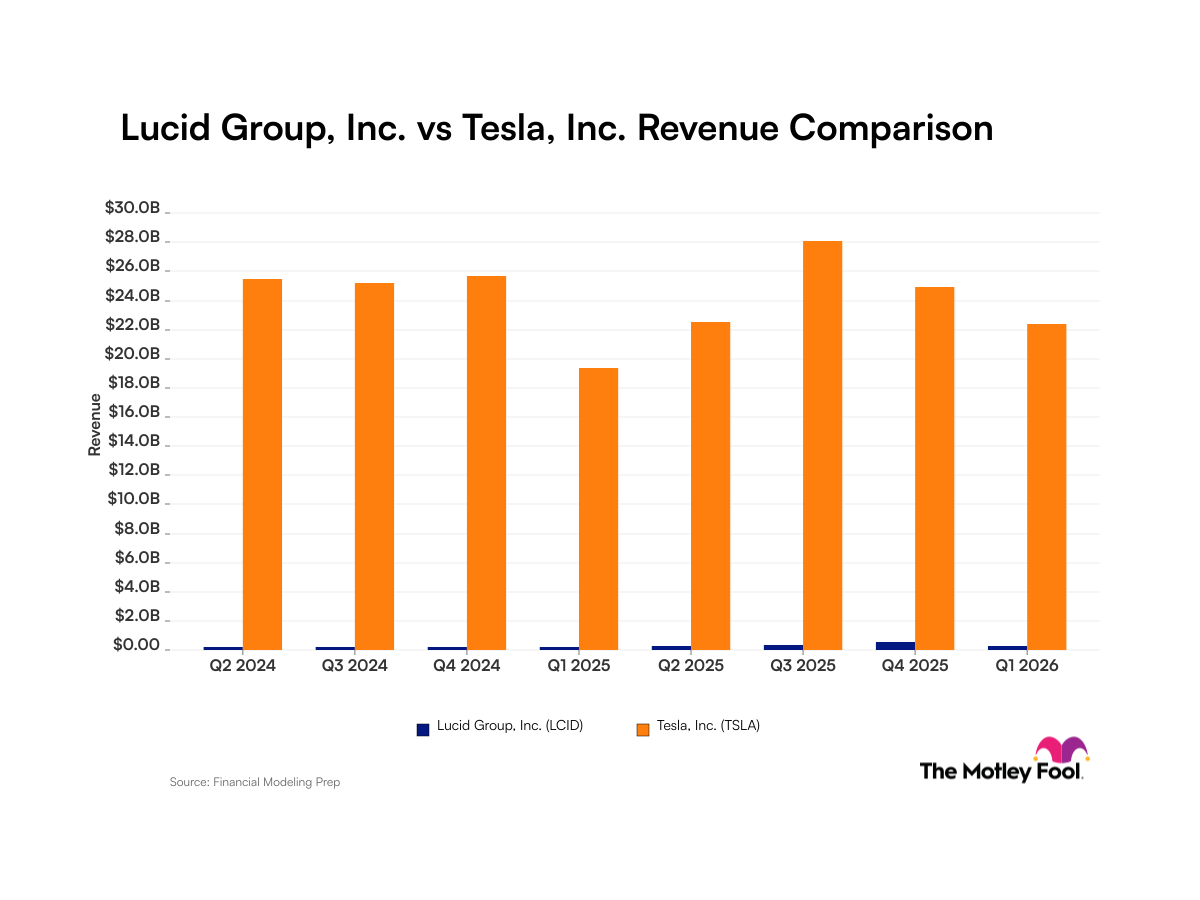

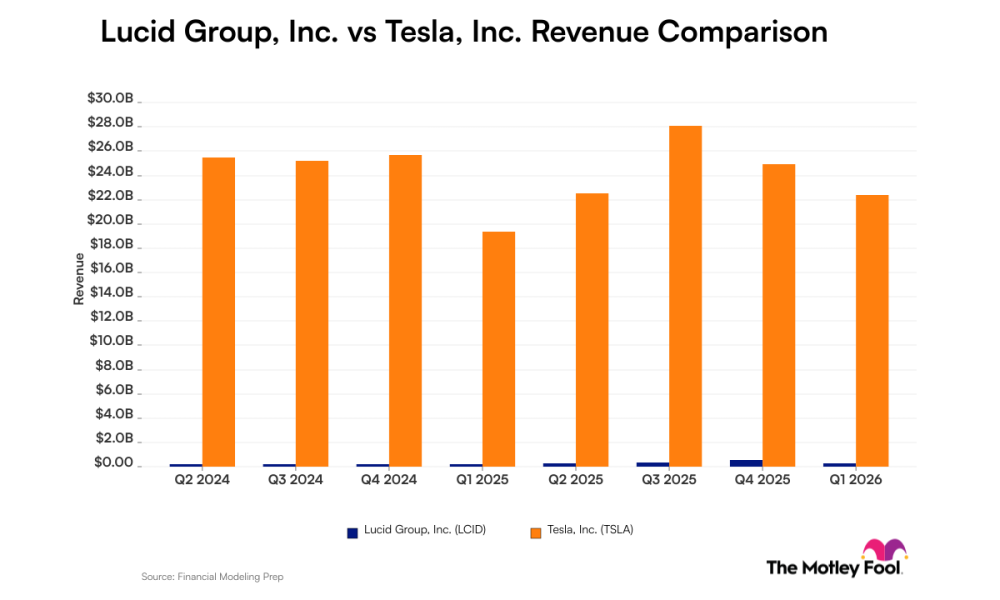

Quarterly Revenue for Lucid and Tesla

| Quarter (Period End) | Lucid Revenue | Tesla Revenue |

|---|---|---|

| Q2 2024 (June 2024) | $200.6 million | $25.5 billion |

| Q3 2024 (Sept. 2024) | $200.0 million | $25.2 billion |

| Q4 2024 (Dec. 2024) | $234.5 million | $25.7 billion |

| Q1 2025 (March 2025) | $235.0 million | $19.3 billion |

| Q2 2025 (June 2025) | $259.4 million | $22.5 billion |

| Q3 2025 (Sept. 2025) | $336.6 million | $28.1 billion |

| Q4 2025 (Dec. 2025) | $522.7 million | $24.9 billion |

| Q1 2026 (March 2026) | $282.5 million | $22.4 billion |

Data source: Company filings.

Foolish Take

The vast difference in revenue between the two EV maker is clear. Revenue isn’t profitability, but Tesla is the far leader here as well. Lucid is still in the early stages of growing its EV business, but it is facing major headwinds.

Demand has waned and overall EV sales growth rates have slowed. That has led to Lucid reporting increased losses and counting on its vast cash holdings to remain viable. That cash has mostly come from investments by its largest shareholder, the Saudi Arabian Public Investment Fund (PIF). Lucid’s current position is untenable, and it is counting on a vast increase in sales from its latest Gravity SUV offering and a new robotaxi partnership with Uber Technologies (UBER +0.93%).

Tesla stock also has many risks as it increasingly focuses on its own self-driving technology as well as energy storage products. Tesla’s scale gives it cash flow to invest in those newer product segments, however. It’s unlikely that Lucid will be “the next Tesla,” and there is real concern for its long-term survival. Tesla investors are counting on its technology advantages, and that’s where progress needs to be monitored.

Data source: Company filings. Data as of May 10, 2026.