Finance

Amazon’s AI Chip Backlog Stands at a Massive $225 Billion. That’s Great News for This Semiconductor Stock That Has Doubled in 2026

Major hyperscalers and cloud computing companies have been busy developing in-house artificial intelligence (AI) chips in recent years in a bid to reduce their reliance on Nvidia and lower the operating costs of AI data centers.

Amazon (NASDAQ: AMZN) is one such company that has been designing its own chips to run internal AI workloads in its data centers. However, the performance and cost efficiency advantages delivered by Amazon’s custom AI processors mean its chips are witnessing healthy demand from third parties as well.

In fact, Amazon is quietly turning out to be a major player in the AI chip market. Let’s take a closer look at the scale of Amazon’s AI chip business before checking out a high-flying semiconductor stock that could help you benefit from the rapid growth that the tech giant is witnessing in AI chips.

The strong demand for Amazon’s custom artificial intelligence processors will be a tailwind for its semiconductor design partner.

Major hyperscalers and cloud computing companies have been busy developing in-house artificial intelligence (AI) chips in recent years in a bid to reduce their reliance on Nvidia and lower the operating costs of AI data centers.

Amazon (AMZN 0.20%) is one such company that has been designing its own chips to run internal AI workloads in its data centers. However, the performance and cost efficiency advantages delivered by Amazon’s custom AI processors mean its chips are witnessing healthy demand from third parties as well.

In fact, Amazon is quietly turning out to be a major player in the AI chip market. Let’s take a closer look at the scale of Amazon’s AI chip business before checking out a high-flying semiconductor stock that could help you benefit from the rapid growth that the tech giant is witnessing in AI chips.

Image source: Amazon

Amazon’s AI chip business is taking off

Amazon’s custom AI accelerators, known as Trainium, are in terrific demand. This is evident from the comments made by CEO Andy Jassy on the company’s recent earnings call. Jassy noted:

Our chips business continues to grow rapidly and is larger than what a lot of folks thought. We saw nearly 40% quarter over quarter growth in Q1, and our annual revenue run rate is now over $20 billion and growing triple-digit percentages year over year, but this somewhat masks the size.

If our chips business was a stand-alone business and sold chips produced this year to AWS and other third parties as other leading chip companies do, our annual revenue run rate would be $50 billion.

Jassy added that Amazon has become one of the top three data center chip companies in the world. The remarkable growth that the Magnificent Seven company has been witnessing in this segment is fueled by the improving performance profile of its Trainium chips. The company claims that its latest Trainium3 chip is almost fully sold out. That’s not surprising as Trainium3 reportedly offers 30%-40% better price-to-performance ratio when compared to the previous generation Trainium2 chip.

Amazon

Today’s Change

(-0.20%) $-0.55

Current Price

$272.13

What’s more, Amazon claims that the Trainium2 chip itself offers a 30% higher price-to-performance than graphics processing units (GPUs). These performance advantages explain why Amazon has almost fully sold out its Trainium3 chips. What’s more, customers have started reserving the company’s next-generation Trainium4 chips, which are still a year and a half away from launch.

Top AI companies such as Anthropic and OpenAI are using Amazon’s custom processors. Meanwhile, Meta Platforms is poised to deploy Amazon’s Graviton server central processing units (CPUs) in its data centers to “run the CPU-intensive workloads behind agentic AI with the performance and efficiency they need at their scale.”

Such a solid customer base and the incredible demand for Amazon’s AI chips explain why the company says that it has “over $225 billion in revenue commitments for Trainium.” So, Amazon’s AI chip business is poised for remarkable growth going forward, and this is great news for Marvell Technology (MRVL +0.80%) investors.

Marvell Technology will be a big beneficiary of Amazon’s huge AI chip backlog

Amazon designs its custom AI chips in collaboration with Marvell Technology. The two companies deepened their existing relationship in December 2024 for five years, with Marvell designing custom AI processors and networking components for Amazon.

Marvell Technology

Today’s Change

(0.80%) $1.37

Current Price

$171.50

This partnership is one of the key reasons why Marvell has been enjoying solid growth. The company’s revenue in fiscal 2026 (which ended on Jan. 31) increased by 42% year over year to $8.2 billion. Its earnings shot up by 81% last year to $2.84 per share. The company’s strong ties with Amazon should help it sustain healthy growth in the future as well.

The chip designer sees its data center revenue growing by 40% in the current fiscal year, while overall revenue is expected to increase by 30%. Even better, Marvell expects 40% revenue growth in fiscal 2028. The company expects to deliver at least $5.00 in earnings per share in the next fiscal year.

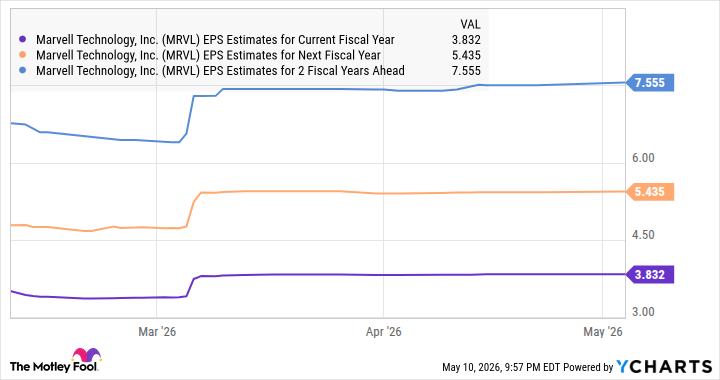

Consensus estimates suggest that Marvell could sustain strong earnings growth beyond the next fiscal year.

MRVL EPS Estimates for Current Fiscal Year data by YCharts

It is easy to see why analysts are bullish about Marvell’s prospects. The company noted on its March earnings call that it has “20-plus design wins or product sockets that are either in production or going into production” across multiple customers in fiscal 2028 and fiscal 2029. All this suggests that Marvell is in a solid position to capitalize on the secular growth of the custom AI processor market, which is poised to clock a compound annual growth rate of 27% through 2033, according to Bloomberg.

So, don’t be surprised to see this semiconductor stock heading higher in the future. Marvell stock has doubled in 2026 as of this writing. If it indeed achieves $7.56 in earnings per share in fiscal 2029 (in line with the consensus estimate seen in the chart) and trades at 43 times earnings at that time (in line with the tech-laden Nasdaq Composite index’s earnings multiple), its stock price could reach $325.

That suggests potential upside of 91%. So, investors can still consider buying this AI stock as it can deliver substantial upside even after the impressive gains it has clocked this year.