Finance

3 Reasons It’s Not Too Late to Buy Eli Lilly Stock

Eli Lilly (NYSE: LLY) continues to prove the doubters wrong. Despite fears that the company’s shares are overvalued, and that stiff competition in the GLP-1 market will eventually catch up to the drugmaker, Eli Lilly posted yet another excellent performance during the first quarter that breathed new life into the stock. Eli Lilly’s shares jumped by about 10% after its earnings release on April 30. However, Eli Lilly’s shares are still down by 10% to date, and at current levels, it isn’t too late to invest in the company. Here are three reasons why.

Image source: The Motley Fool.

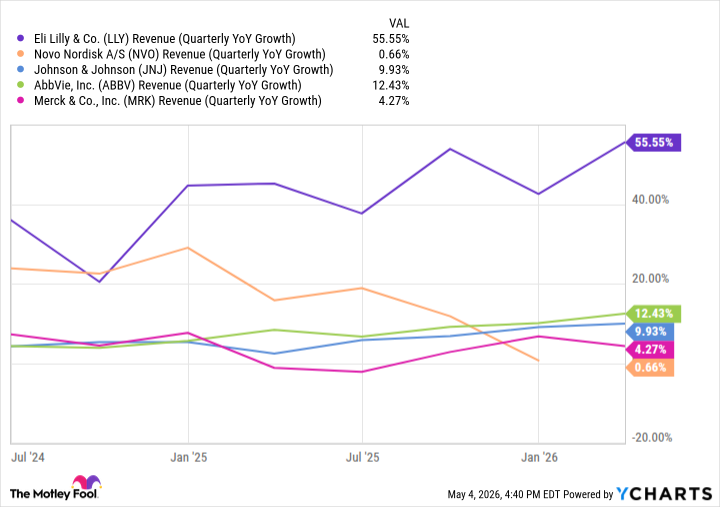

In the first quarter, Eli Lilly’s revenue of $19.8 billion grew by 56% year over year. Top-line growth rates of this caliber are exceedingly rare for major pharmaceutical companies, but not so much for Eli Lilly. The company’s sales have consistently increased at an incredible clip over the past couple of years compared to those of its similarly sized peers.

The company still has a strong lead in its core therapeutic area.

Eli Lilly (LLY +0.44%) continues to prove the doubters wrong. Despite fears that the company’s shares are overvalued, and that stiff competition in the GLP-1 market will eventually catch up to the drugmaker, Eli Lilly posted yet another excellent performance during the first quarter that breathed new life into the stock. Eli Lilly’s shares jumped by about 10% after its earnings release on April 30. However, Eli Lilly’s shares are still down by 10% to date, and at current levels, it isn’t too late to invest in the company. Here are three reasons why.

Image source: The Motley Fool.

1. A booming GLP-1 business

In the first quarter, Eli Lilly’s revenue of $19.8 billion grew by 56% year over year. Top-line growth rates of this caliber are exceedingly rare for major pharmaceutical companies, but not so much for Eli Lilly. The company’s sales have consistently increased at an incredible clip over the past couple of years compared to those of its similarly sized peers.

LLY Revenue (Quarterly YoY Growth) data by YCharts

Earnings growth is equally impressive. Eli Lilly posted adjusted earnings per share of $8.55, up 156% compared to the year-ago period. To no one’s surprise, Eli Lilly’s GLP-1 portfolio, which includes Mounjaro for diabetes and Zepbound for obesity, did most of the heavy lifting. Sales of Mounjaro climbed 125% year over year to $8.7 billion, with revenue from Zepbound landing at $4.2 billion, 80% higher than Q1 2025.

Clearly, there is an incredible demand for Eli Lilly’s drugs. And here’s the good news: Eli Lilly’s core business could continue driving solid growth for a while. The company earned approval for Foundayo — an oral GLP-1 medicine for weight loss — in early April. This therapy is expanding Eli Lilly’s market. As management said, 80% of people on Foundayo are new patients who hadn’t taken GLP-1 medicines before, perhaps because they disliked injections, because of the high monthly cost of these therapies, or for other reasons. The addition of Foundayo will help boost an already high-performing business.

Eli Lilly

Today’s Change

(0.44%) $4.27

Current Price

$967.60

2. Positive regulatory developments

On April 30, the U.S. Food and Drug Administration (FDA) announced a proposal that would remove tirzepatide (the active ingredient in Mounjaro and Zepbound) from a list it maintains of pharmaceutical ingredients for which it deems there is a clinical need. Long story short, FDA-registered 503B outsourcing facilities can compound drugs at scale without patient-specific prescriptions, provided certain conditions are met, such as when a drug is in shortage or when the drug bulk substance is on the aforementioned list.

Some telehealth companies have used this pathway to offer compounded versions of tirzepatide to patients at much lower prices than the branded versions. This has been a thorn in Eli Lilly’s side, as cheaper compounded versions of tirzepatide have flooded the market, somewhat eroding its pricing power. Eli Lilly has attempted to address this problem, but so far it has had little success. Provided the FDA finalizes this proposal, it could be yet another boost to the company’s GLP-1 business. Investors should carefully monitor that.

3. Sales are growing fast elsewhere

Although Eli Lilly is currently primarily a GLP-1 company, the drugmaker also has several other products in other areas whose sales are growing rapidly. In the first quarter, revenue from Jaypirca, a cancer therapy, jumped 79% year over year to $165 million. Sales of Ebglyss, an eczema treatment, Alzheimer’s disease medicine Kisunla, and ulcerative colitis drug Omvoh more than doubled. True, these therapies account for a small percentage of Eli Lilly’s total revenue right now, as its GLP-1 products dominate.

However, Eli Lilly’s ability to launch products in other areas that can also exceed $1 billion in annual sales, which some analysts expect for all four of these therapies, is noteworthy. Eli Lilly is doubling down. The company has worked hard to expand its pipeline through acquisitions over the past few years. And moving forward, we should see significant clinical progress for the company in areas beyond GLP-1, which may help Eli Lilly perform well despite mounting competition in its core therapeutic area.

The company’s shares aren’t cheap — Eli Lilly is trading at 28.5x forward earnings, compared to the average of 16.5x for healthcare stocks. But considering how fast the revenue and earnings are growing, Eli Lilly is worth the premium. Investors who purchase its shares today may still see strong returns through the next five years.