Few companies stand as centrally as Sandisk (NASDAQ: SNDK) in artificial intelligence (AI) ecosystems. As a pure-play leader in NAND flash memory and advanced storage solutions, Sandisk designs and manufactures high-capacity components that form the foundation of AI data centers.

Unlike traditional hard drives, Sandisk’s NAND technology delivers the low-latency performance required for training large language models, deploying inference at scale, and supporting massive volumes of unstructured data generated by AI workloads.

These dynamics position Sandisk not as a peripheral equipment supplier, but as a critical enabler of AI architectures, where each new breakthrough model and application demands ever-greater storage density and speed.

Sandisk stock has surged more than 500% so far in 2026, but the stock could still carry explosive gains.

Few companies stand as centrally as Sandisk (SNDK +0.15%) in artificial intelligence (AI) ecosystems. As a pure-play leader in NAND flash memory and advanced storage solutions, Sandisk designs and manufactures high-capacity components that form the foundation of AI data centers.

Unlike traditional hard drives, Sandisk’s NAND technology delivers the low-latency performance required for training large language models, deploying inference at scale, and supporting massive volumes of unstructured data generated by AI workloads.

These dynamics position Sandisk not as a peripheral equipment supplier, but as a critical enabler of AI architectures, where each new breakthrough model and application demands ever-greater storage density and speed.

Sandisk

Today’s Change

(0.15%) $2.42

Current Price

$1564.76

Analyzing Sandisk’s revenue and earnings growth

Demand for Sandisk’s NAND-based storage solutions has surged as hyperscalers and cloud providers race to build out infrastructure capable of handling AI’s appetite for data.

Recent quarterly results reflect these tailwinds. During the company’s fiscal third quarter (ended April 3), revenue surged 251% year over year to $5.9 billion. Sandisk’s growth was fueled by impressive performances across its data center and edge devices segments, where demand for its solid-state drive (SSD) portfolio and shift toward AI-enhanced PCs and smartphones are accelerating. Earnings have followed suit, with gross margins expanding thanks to the company’s pricing power.

While memory and storage were long considered cyclical industries tied to consumer electronics upgrades, Sandisk’s trajectory appears to be tied to a secular AI narrative featuring long-term contracts from major developers — providing visibility well into the future.

This structural shift has propelled Sandisk’s stock to extraordinary gains — with shares surging more than 500% so far in 2026, making Sandisk the top-performing company in the Nasdaq-100.

Image source: Getty Images.

Sandisk is cleaning up its balance sheet

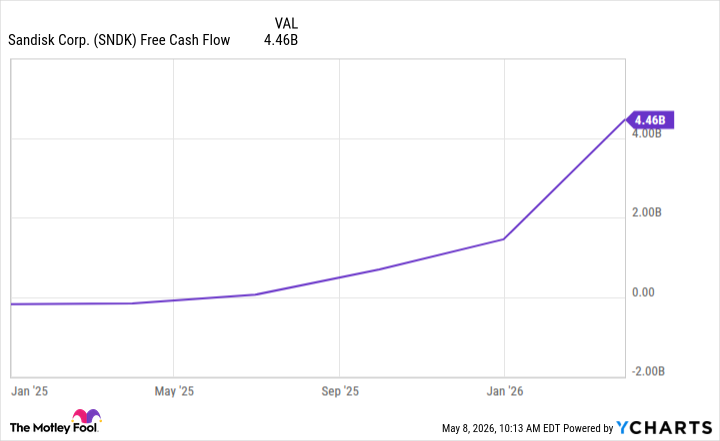

With profitability accelerating, Sandisk now has the financial flexibility to implement a disciplined capital allocation strategy centered on consistent free cash flow generation. Over the last year, the company produced $4.5 billion in free cash flow annually.

SNDK Free Cash Flow data by YCharts

This has allowed Sandisk to fund internal investments while also steadily deleveraging. At the end of its fiscal third quarter, Sandisk held zero debt on its balance sheet.

Sandisk just announced a $6 billion stock buyback

Building on the momentum of paying down debt, Sandisk recently authorized a $6 billion stock repurchase program. This move signals deep conviction in its trajectory and serves a dual purpose. First, the buyback demonstrates management’s belief that shares remain undervalued even after their meteoric run-up. Second, it represents a direct counter to the long-standing narrative that memory and storage are hopelessly cyclical.

Image source: Getty Images.

In an AI landscape where storage needs compound with every new model deployment, Sandisk’s leadership appears durable — backed by secular demand rather than boom-and-bust volatility. In my eyes, the decision to use excess cash flow to repurchase shares effectively puts the cyclical label to rest and reinforces the company’s evolution to a growth-oriented business.

Taken together, Sandisk makes a compelling addition to AI-themed portfolios. The company’s technology has become indispensable, the financial profile is strengthening, and management’s capital returns reflect prudent optimism. For investors seeking exposure to the AI infrastructure era, Sandisk stands out as a high-conviction opportunity with the potential to deliver sustained upside in the years ahead.