This is shaping up to be a history-making month for Wall Street. Earlier this month, the benchmark S&P 500 (SNPINDEX: ^GSPC) and tech-stock-dependent Nasdaq Composite (NASDAQINDEX: ^IXIC) both soared to record highs, with the ageless Dow Jones Industrial Average (DJINDICES: ^DJI) perched one solid up day away from joining its peers.

Meanwhile, Jerome Powell will serve his final day as Fed chair on May 15. President Donald Trump’s nominee to succeed Powell, Kevin Warsh, cleared a key hurdle by receiving a majority vote from the Senate Banking Committee and is expected to secure the necessary votes in the Senate for confirmation. He’s on track to become the 17th head of the Fed.

Fed Chair Jerome Powell and President Trump have been feuding over interest rates for over a year. Image source: Official White House Photo by Daniel Torok.

Not even Wall Street saw this as a possibility three months ago.

This is shaping up to be a history-making month for Wall Street. Earlier this month, the benchmark S&P 500 (^GSPC +0.84%) and tech-stock-dependent Nasdaq Composite (^IXIC +1.71%) both soared to record highs, with the ageless Dow Jones Industrial Average (^DJI +0.02%) perched one solid up day away from joining its peers.

Meanwhile, Jerome Powell will serve his final day as Fed chair on May 15. President Donald Trump’s nominee to succeed Powell, Kevin Warsh, cleared a key hurdle by receiving a majority vote from the Senate Banking Committee and is expected to secure the necessary votes in the Senate for confirmation. He’s on track to become the 17th head of the Fed.

Fed Chair Jerome Powell and President Trump have been feuding over interest rates for over a year. Image source: Official White House Photo by Daniel Torok.

While this is a change that couldn’t come soon enough for Donald Trump, it’s a shift that may ultimately backfire on the president and force the central bank’s hand in a way that no one — not even Wall Street — saw coming three months ago.

The Trump vs. Powell feud has been ongoing for more than a year

Sitting presidents are responsible for nominating the Federal Reserve chair. Since Trump was inaugurated for his second, non-consecutive term on Jan. 20, 2025, he and Jerome Powell have been vocally feuding.

The president has made clear on several occasions that he’d like to see Powell and the Federal Open Market Committee (FOMC) aggressively cut interest rates. The FOMC is the 12-person body that sets the nation’s monetary policy.

Specifically, the president has called on Powell and the FOMC to cut the federal funds target rate to 1% or lower. Slashing interest rates would likely encourage corporate borrowing, leading to increased hiring, acquisitions, and capital spent on innovation. Lower borrowing costs could potentially reverse a modest uptick in the unemployment rate over the last few years.

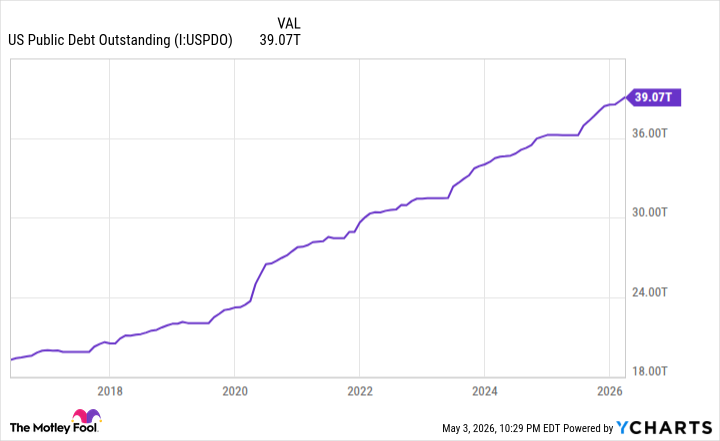

US Public Debt Outstanding data by YCharts.

Perhaps more importantly, Donald Trump recognizes that lower lending rates would make it easier for the U.S. to service its $39 trillion in national debt. Federal deficits have totaled at least $1.38 trillion every fiscal year since 2020 (the government’s fiscal year ends on Sept. 30).

Meanwhile, Fed Chair Powell has been adamant that the FOMC will base its monetary policy decisions solely on economic data, not political opinions. Powell has pointed to the price stickiness of President Trump’s tariffs in the goods sector as one of several reasons the FOMC is not acting more aggressively to ease rates.

In other words, the writing has been on the wall for quite some time that Powell wouldn’t be nominated for a third term. But just because Trump is getting his wish for change at the Fed’s top position, it doesn’t mean he’s going to receive his desired result of lower interest rates with Kevin Warsh in charge.

President Trump overseeing Operation Epic Fury against Iran. Image source: Official White House Photo by Daniel Torok.

President Trump’s decision is likely to force the Fed’s hand (and Wall Street won’t be happy)

When Warsh takes the helm after May 15, he’ll be leading perhaps the most divided FOMC in history. Powell’s final FOMC meeting as Fed chair featured four dissents among 12 votes — the highest number of dissents in 34 years!

But it’s not the fractured FOMC that’s the biggest threat to President Trump’s wish for lower interest rates. It’s the president’s own actions regarding the Iran war that may ultimately force the Fed to act.

On Feb. 28, Trump gave the order for U.S. military forces, along with Israel, to commence attacks against Iran. Shortly after these military operations began, Iran closed the Strait of Hormuz to virtually all commercial vessels, thereby throwing 20 million barrels of liquid petroleum into limbo each day! This accounts for approximately 20% of the world’s demand and represents the largest energy supply disruption in modern history.

This historic supply shock has been quickly factored into energy prices. Gas prices have soared at their fastest pace in three decades.

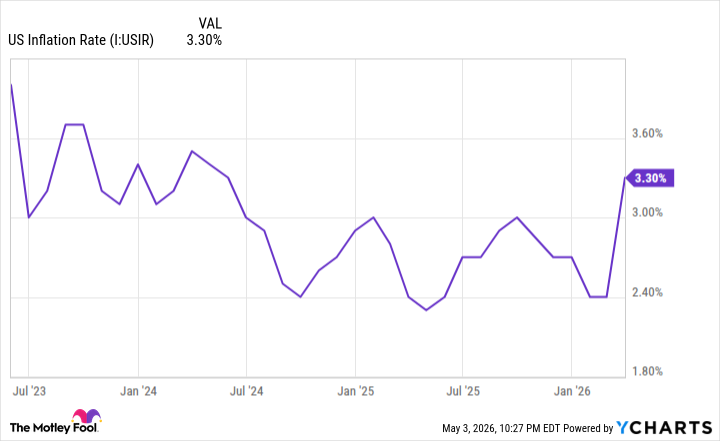

However, the inflationary effects of the Iran war are, arguably, just getting started. While these effects are most visible at the fuel pump, the impact on transportation and production costs for businesses often takes several months to be reflected. Once these effects are felt, U.S. inflation can push even higher.

In February, before the effects of the Iran war were visible in economic data, trailing 12-month (TTM) inflation came in at 2.4%. In March, TTM inflation jumped 90 basis points to 3.3%. According to estimates from the Cleveland Fed’s Inflation Nowcasting tool, TTM inflation is projected to rise to 3.56% in April and 3.88% in May. That’s a nearly 150-basis-point increase in three months — and it may force the Fed’s hand.

US Inflation Rate data by YCharts.

Three of the dissenting opinions at the FOMC’s April 29 meeting opposed the use of an easing bias in the central bank’s statement. In other words, a quarter of the FOMC’s voting members have no desire to continue lowering interest rates as inflation notably jumps. As inflation rises, the FOMC may have no choice but to increase the federal funds target rate to stabilize prices.

Keep in mind that Kevin Warsh was known as a hawk for his stance on price stability during the financial crisis. As a former voting member of the FOMC, Warsh argued against lowering interest rates, even as the unemployment rate soared. If Warsh’s past is any indication of how he’ll vote in the future, there’s a growing likelihood that borrowing costs will rise, not decline, before year’s end.

Collectively, this portends trouble for a pricey stock market that entered 2026 expecting several rate cuts. With the prospect of lower lending rates essentially off the table, investors may be forced to come to terms with historically high stock valuations that can no longer be supported. It’s a no-win scenario for Wall Street.